Why the Balanced Scorecard Doesn't Fit the Public Sector

BLOG ARCHIVE

(Originally published 20 May 2010)

The balanced scorecard (BSC) has been marketed aggressively to governments as a framework for public sector performance measurement. But the BSC is not, and never was, an appropriate performance measurement framework for government. It was developed as a private sector framework and, notwithstanding superficial adjustment to the public sector context, remains fundamentally private sector in nature.

There is only one performance measurement framework appropriate to government: the results chain, also known as the “logical framework” or “program logic”. This is the framework which uses the concepts of outcomes, outputs, activities/processes and inputs to classify performance measures. The results chain recognizes, in a way which no other performance measurement framework does, the distinctive nature of the public sector. It does so, most of all, in its focus on outcomes – overarching non-financial objectives such as national security, improved health, environmental conservation and high employment. This is fundamentally different from the private sector focus on financial results and products (outputs).

Like other private sector frameworks, the BSC lacks the clear outcomes focus of the results chain, and is focused on performance measurement challenges which are not the most important challenges in a government context.

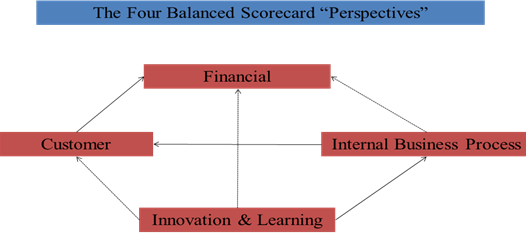

The BSC is one of a number of private sector frameworks developed as an antidote to near-exclusive reliance by businesses upon financial performance measures (particularly, profit and shareprice). But this was not because the BSC in any way disputed the primacy of profits for business. The central BSC theme is that measures of present financial performance measurements are insufficient because they are essentially backward looking and do not capture the determinants of future financial performance. In order to capture the drivers of future business success, the BSC supplements financial indicators with three other categories of indicators, grouped in “perspectives”. These are: customer indicators (indicating customer satisfaction, loyalty etc); internal process indicators (efficiency, etc); and “innovation and learning” indicators. The primacy of the financial perspective was explicitly recognized, with the other three perspectives viewed as subordinate and contributing to the financial perspective.

The Standard Private Sector Balanced Scorecard

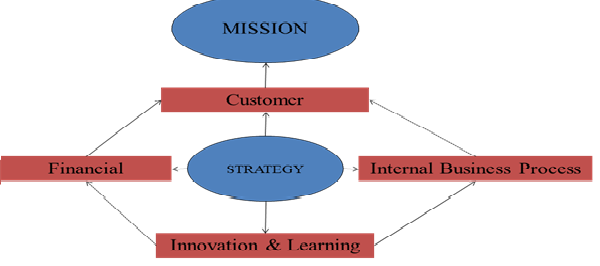

The BSC’s originators eventually recognized the inappropriateness of the standard version of the scorecard for government, and proposed a modified version which was intended to acknowledge the primacy of non-financial objectives. Strategic planning was grafted onto the scorecard, with organizational mission taking the place of profit as the overarching objective and strategy made the guide to performance indicator selection. The other change was the ranking of the “perspectives”, with the customer perspective placed above all others, based on the reasoning that customer satisfaction was central to the achievement of the organizational mission.

The Government Balanced Scorecard

The modified BSC suffers from all the problems inherent in seeking to use strategic planning models as the performance indicator framework: in particular, the imprecision of the mission concept, the inappropriateness of focusing on customers instead of upon outcomes, and the mistaken notion that all indicators should be drawn from the formal strategic plan. The use of the BSC can, as a result, blur rather than reinforce the outcomes focus which should dominate government performance measurement.

An example of the type of confused thinking to which the focus on customers rather than outcomes has led can be seen in the writings of one influential exponent of the public sector BSC:

Establishing the real customer in many ways depends on your perspective. In the public sector the legislative body that provides funding is a logical choice, as is the group you serve. However, think about that group you “serve.” Would law enforcement agencies consider the criminals they arrest their customer? You could probably make a case for that. Conversely, many would argue that constituents are the ultimate beneficiaries of policing activities and are therefore the real customers. Fortunately, the Balanced Scorecard doesn’t force you to make this difficult decision. Including all customers is permissible and possible using the public sector Scorecard framework. (Niven: 2003.)

An outcomes focus clarifies the position. The primary intended outcome of law enforcement is reduced crime, and it is complete nonsense to consider criminals as “customers” of police services. No question of “perspective” arises. Renaming the “customer” perspective the “stakeholder” perspective – as some BSC exponents have done – hardly helps much with this problem. Criminals are no more stakeholders in police services than they are customers. And formal consultation with organized crime in the development of police strategic plans and performance indicators is something which (presumably) no-one would advocate.

Another notable feature of the public sector balanced scorecard is the insistence on retaining a separate financial perspective. In the private sector BSC, the meaning of the financial perspective is clear – it is first and foremost about profit. But what is the financial perspective supposed to mean in a government context? BSC exponents usually suggest that it becomes a category for efficiency measures. But this has the peculiar consequence of separating efficiency indicators from measures of quantity and quality, which would remain under the customer category. But surely it is better to adopt the results chain approach of viewing quantity, quality and efficiency indicators of outputs together? Take another example of the type of indicator which BSC exponents allocate to the financial perspective: a measure of value of overpayments to recipients of government transfer payments (e.g. agricultural subsidies). Again, however, what is the logic in separating financial measures of this particular process from non-financial measures such as the timeliness of payments? Other than in the case of government business enterprises, or government as a whole (for which profit measures are very important), cordoning off financial indicators as a separate “perspective” makes very little sense.

The BSC “innovation and learning” perspective has two main elements. One is human and organizational resources, which is captured in the results chain framework under the resources category. The other is technological innovation. Raising technological innovation to the level of a perspective makes sense if you are a business in, say, consumer electronics, where those who come up with blockbuster product –the Iphone, or the walkman in earlier times – sweep the field and drive others out of business. In most government services – think, for example, education, garbage collection and environmental regulation – product innovation is much less important than process innovation – that is, changes in the process of production to reduce the costs of production. They are mainly what Mark Moor refers to as “innovations and investments to improve operational performance”. It is not at all clear that it makes sense to separate innovation indicators in this context, rather than keeping them linked with output and activity indicators. In practice, the “innovation and learning” indicators in balance scorecards developed by government organizations tend to have few innovation indication, and to feature mainly human resources and organizational indicators.

The biggest flaw with the BSC in government is that it addresses the wrong problem. The BSC was developed to address the problem that business corporations could measure their results – meaning, for them, financial results – relatively easily, but in doing so were not measuring the determinants of future results. This is not, and never has been, the primary performance measurement problem in government. For government, measuring results and, more generally, focusing management on results, is the key problem. Any performance measurement framework which does not give that problem primary attention is missing the point.

References:

Paul Niven (2003), The Balanced Scorecard Step-by-Step for Government and Non-Profits.

Mark Moor (2003), The Public Value Scorecard, Working Paper #18, Kennedy School of Government, Harvard University.